Periodic Savings and Investment Plan - The Goal Getter

The Periodic Savings and Investment Plan (PSIP) is a tool that helps you put money aside on a regular basis.

For your short- and medium-term projects, the Goal Getter plans can make a difference in achieving your savings objectives.

For your long-term project, the Investment Plan (PAC) might better suit your needs.

The investment plan (PAC)

The Investment Plan is a flexible plan that helps you achieve your savings objectives in mutual funds.

It is simple: a predetermined amount of money is taken from your account and invested in mutual funds, on a regular basis and at the frequency of your choice. Your Investment Plan can be modified at any time depending on your needs.

| CHARACTERISTICS2 | |

|---|---|

| Eligible investment | Mutual funds1 |

| Minimum amount | $25 per week $50 per month |

| Contribution frequency | Weekly Bi-weekly Bi-monthly (On the 1st and 15th of each month) Monthly |

| Modifications allowed | Frequency of contributions Amount of contributions Cancellation of contributions |

Advantages

Ease: It’s much simpler to put aside a small amount on a regular basis than a large one-time amount. As your payments are made automatically, you can grow your savings without thinking about it.

Flexibility: Investment Plan offers you more flexibility. You choose how much and how often you want to save. Modify the program or cancel it altogether at any time.

Efficiency: By investing periodically in mutual funds, you reduce the average acquisition cost of your shares. In fact, you buy more shares when prices decline and you buy less when prices are on the rise.

| ADVANTAGES OF PERODICAL ACQUISITIONS: - average acquisition cost + number of shares acquired |

||

|---|---|---|

| Periodical acquisitions (1/month) |

Lump-sum acquisition (1 in January) |

|

| Total investment | $1,800 | $1,800 |

| Average acquisition price | $10,56 | $12,00 |

| Number of shares acquired | 170,36 | 150,00 |

| Market value | $2,385.04 | $2,100.00 |

| $285.04 variation | ||

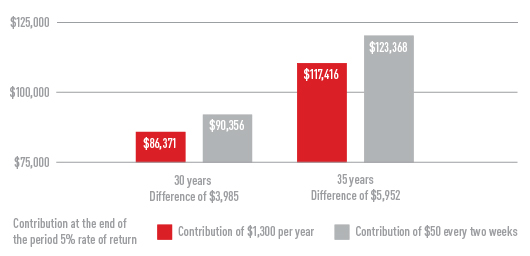

When it comes to planning your retirement, systematic savings can help your nest egg grow every month, tax-free. The graph below demonstrates the advantages of monthly RR SP contributions over a single annual lump-sum at the end of the year. For example, an investor who begins contributing at 25 could pocket an extra $5,952 to retire at age 60.

| IMPACT OF A CONTRIBUTION EVERY TWO WEEKS COMPARED TO A YEARLY CONTRIBUTION3 |

|---|

|

Summary

This investment strategy is suited for you if:

- You wish to foster good saving habits;

- You wish to save some money to realize a long-term project;

- You are seeking simple and efficient solutions to save money;

- You wish to limit the impact of market fluctuations on your mutual funds portfolio.

This investment strategy is not suited for you if:

- You do not have a stable income allowing you to make regular payments.

- Mutual funds do not suit your investor’s profile.

*Trademark of Visa Int., used under license.

Legal notice

Existing investment accounts are offered by Laurentian Bank of Canada (“Laurentian Bank”) or LBC Financial Services Inc. (“LBCFS”). LBCFS is a wholly-owned subsidiary of Laurentian Bank and a legal entity, distinct from Laurentian Bank, B2B Trustco, and any issuers or mutual fund companies whose products it distributes. All new investment account opening must be through LBCFS. A Laurentian Bank advisor is also a licensed LBCFS mutual fund representative. LBCFS’s liability is limited to the conduct of its representatives in the performance of their duties for LBCFS.

1. An investment in a fund may give rise to sales and maintenance commissions, management and other fees. Please read the simplified prospectus before making an investment. Mutual funds are not guaranteed investments; their value often fluctuates, and past performance is not an indication of future performance. distributed by LBC Financial Services, a wholly owned subsidiary of Laurentian Bank.

2. Administration fees may apply, however, portfolios of $25,000 or more, or comprised of guaranteed investment certificates only, are free of charge.

3. Fictional example provided solely for information purposes, based on an investment in mutual funds.